If you’re working for a company in Australia and plan to stay here permanently, it’s most likely that about 9.5% of your salary is being paid by your employer towards your Superannuation fund – this is the money you build up over your lifetime and which you’ll use in retirement. This retirement system was set up in the early 1990s as a way to plan for an ageing society as the government didn’t believe it would be able to pay for everyone to get the pension as they had before.

[Note: If this article is a bit difficult for your level please check out this short list of very useful financial terms here]

You can choose to have your Super contributions paid into funds which invest in different asset classes, including property, equities and bonds. Most people can choose the fund that best suits their priorities, values and aversion to risk, and understanding how different asset classes perform can make a big difference over your lifetime. Yet I wonder how many people understand where their money is going. Have you ever studied or read much about personal finance?

Some people feel more comfortable leaving their money with portfolio managers who decide where the money goes and how the asset allocation will be determined, whereas others want to know exactly where their money is going. For example, fund managers don’t always make the right decisions (sometimes they get things wrong) and there might be some industries or companies that you wouldn’t want to support (like investing in a company that profits from war or that doesn’t support clean energy, for example).

Some English students say “this is a boring topic” or “I don’t care about the markets” but if you want to have more money over your lifetime and make informed decisions, I think it’s good to read a lot and get educated on where you can put your money.

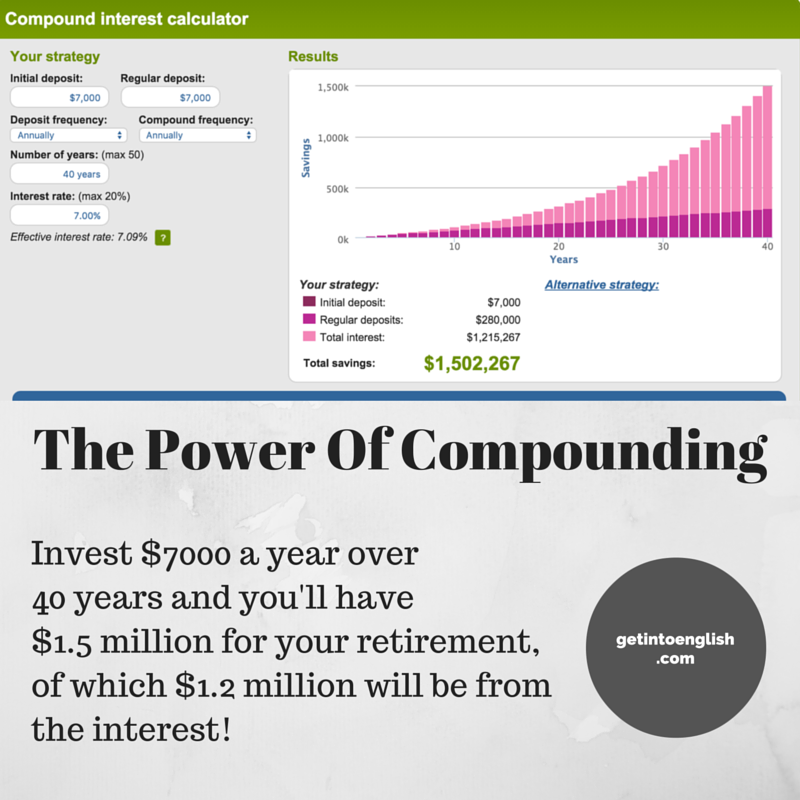

If you still think this is a “boring” topic, check this graph out below. Let’s say you’re working as a waiter and you’re able to put away $7000 a year. This could be either from your employer contributions into Superannuation or from your own voluntary investing (of course you can invest normally during your life outside of your Superannuation fund).

I think in Australia investing $5000-$7000 a year is doable, assuming you don’t have any particular challenging circumstances like having a major disability or illness or having a especially difficult situation. I understand that times are tough for some, but if you track your expenses you’d be surprised where you can find some areas to make some savings. For example, when I was in Prague I often had 2-3 coffees a day and a bottle of water to go with it. Some days I even had 3 or 4 coffees. That works out to a crazy 43000 CZK or 2500 Aussie dollars per annum!

Maybe you’re thinking: “Hey David, I want to have a life here! I want to have my daily coffee/cigarette/drink.” That’s fine, though life is about finding that balance between enjoying what you have now and making decisions today to help you enjoy life more tomorrow.

As you can see from the graph below, and based on historical data, someone who invests wisely over their working life could have well over a million dollars by the time they retire, most of which would be money they make from compound interest (nb if you’re based in another country this principle is the same but the amount might be lower or higher depending on how much you’re making and your country’s economy).

Basic Investment Vocabulary

Asset class

Different asset classes include equities (stocks and shares), fixed income (bonds), and property.

Asset allocation

To allocate v. is used a lot in business and economics. It refers to the way something is to be officially divided or given to a particular purpose.

Asset allocation refers to what extent you should invest in each asset class. One possible asset allocation could be 40% in shares, 40% in bonds and the remainder in real estate or cash. I know a lawyer back home whose father invests mostly in real estate, and she feels comfortable doing the same as she understands it. Other people prefer to invest in shares as they are more liquid and if you research a company and feel confident it’s a good business, it could be a good investment without the maintenance costs involved in real estate.

Aversion to risk

How risk-averse you are refers to how much risk you’re prepared to take with your money. If you’re 25 you might be ok to invest more widely. If you’re 58 you might want to sell some of your shares and put them into less volatile assets such as bonds. Usually the older you get the more risk-averse you’ll be, as you won’t want to see your retirement funds go down too much once you’re retired.

A capital gain/capital loss

If you buy shares in a company for $10 000 and then sell them the next year for $20 000, you’ve made a capital gain of $10 000.

On the other hand, if the value of the shares goes down and then you decide to sell, you’ve made a capital loss.

Note too that there are special laws regarding the taxation of capital gains. You’ll usually pay CGT (Capital Gains Tax) on gains, though you can usually offset losses.

Collocations:

make | report | offset | a gain/loss

It resulted in a gain/loss of $100.

By the way, offset means to balance the loss of something against a gain somewhere else so that you pay less in tax.

Compound interest

This is a bit like getting “interest on top of interest” each year. Let’s say you get a 10% return on your intial investment of $100. After one year you’ll have $110. This means that next year the interest won’t be calculated on your original $100, but rather the new level of $110.

So your money will grow:

After year one: 110 (= $100 + 10% x $100)

After year two: 121 (= $100 + 10% 110)

Note: I’ve written before that you can apply the magic of compounding to learning English! [click here]

A dividend

If you’ve invested in a company on the stock exchange, it’s possible they’ll pay you a small return on your investment every year in the form of a dividend. In Australia yields (= returns) are often around 3-4% although some companies pay even more. However it’s possible that the payouts are unsustainable and may be cut back. RIO Tinto for example has just decided to end its progressive dividend policy.

A progressive dividend policy is where the company pays either a stable or increasing percentage of its profits towards dividends.

Franking credits

Because companies have already paid company tax on their profits, individual tax payers are given special credits that help reduce their taxable income. These special tax credits are called franking credits.

Investing v. Speculation

If you invest in a company because your taxi driver told you it’ll be a big hit, then this is speculation. You’re investing in this company with the hope that it will rise – it’s a bit like betting. Likewise traders speculate – they buy and sell shares based on the expectation they’ll rise or fall. On the other hand, if you’ve researched a company and believe it offers good long-term value and that it has good financials, then this is an example of investing.

Liquidity

This refers to how quickly or easily an asset can be bought or sold and transferred into cash, without affecting its value. Shares are quite liquid – usually you can sell your shares today and have the funds in 5-7 days. Of course some stocks are less liquid than others (think of a small-cap company which few people want to invest in).

LICs and Mutual Funds

A mutual fund is an investment vehicle that receives money from investors and then seeks to maximise gains in various asset classes. Basically portfolio managers decide where to invest your money, and they will charge a fee for their services. Be careful about choosing a fund that charges high fees: as you can guess from the graph above, a 1% or 2% difference each year over your lifetime could end up costing you tens of thousands of dollars!

An LIC is a Limited Investment Company and it is listed on the Australian Securities Exchange (ASX). It functions in a similar way as a mutual fund in that it chooses where to invest your money. Fees are usually lower and there is generally more transparency.

Summing Up

How to manage money, as well as credit and debt, and where to invest is something that is not generally taught at school. So I think we should do our best to learn more to make better decisions with our money. I’ll no doubt write more on this again soon, as I’d especially like to cover the language of shares and stocks.

Disclaimer: in no way should this article or any content on this website be regarded as any kind of medical, legal, financial or other professional advice.

Hey .

I am really thankful for your great articles .Whenever I have time I read them .They are very beneficial specially business types.

Hi Fatima,

Thanks for visiting! This year I plan to cover many different topics, especially those that are not in the main English coursebooks.

Some readers might find it a bit tough but there’s also this post on useful finance vocabulary http://getintoenglish.com/personal-finance-vocabulary/

Have a nice evening!

David